$19 CHINATECH: RETESTING CYCLE LOWS

What I got right / wrong about China in June: update on the ChinaTech thesis and the country's potential in coming months

Executive Summary

ChinaTech rebounded a whopping 53% while the S&P traded relatively sideways—it is now retesting the March lows

Opportunity to acquire cash-rich, profitable, long-term double-digit growth companies at deep value persists, offering an asymmetric risk-return profile

Improvements in coming months on the COVID (i.e., potential re-opening) and macro front (i.e., increasing stimulus) could have a massive impact on the global economy

This post discusses—implicitly or explicitly—investments in equities (tickers: KWEB, BABA, BIDU, JD, PDD, KC), FX and commodities.

Whatever it takes, with Chinese characteristics

In early June I penned a three-part piece on ChinaTech / internet equities, pounding the table about the opportunity to acquire growth at deep value in China. Some notable takeaways included:

Rare opportunity to acquire cash-rich, profitable, long-term double-digit growth companies at deep value

Perfect storm of regulation, macro, geopolitics and COVID has relentlessly battered China’s technology / internet names, creating an attractive entry point often >70% below cycle peaks

Asymmetric risk-return as the bottom seems in—downside scenario seems largely priced in and already-apparent catalysts and improving drivers offer strong re-rating potential

I argued that on March 16, Vice Premier’s Liu He had “channeled his inner Draghi” to deliver his own “whatever it takes” speech, with Chinese characteristics. This speech “presented a floor on valuations and swiftly boosted the market over the subsequent days”. The bottom seemed to be in.

Oh man, was I wrong about that.

Of course, back then it made fundamental sense (i.e., Chinese authorities speaking in favor of resolutely supporting markets, regulation intensity moderating with the regulation cycle transitioning from its announcement into the implementation stage) and for markets confirmed the view. ChinaTech proceeded to rebound a massive 53%—proxied by the largest ChinaTech ETF (ticker: KWEB)! All of this while the S&P treaded water.

Now ChinaTech is retesting the March lows without any words from Liu He this time. Coincidentally, the 20th National Party Congress (NPC) finished yesterday, where Liu He was dropped.

Today's piece provides a brief summary1 of the ChinaTech thesis alongside an update of the four pillars driving valuations (i.e., regulation, macro, geopolitics and COVID policy). Additionally, I offer my take on how to possibly benefit from this opportunity and explain the impact some of these developments could have on the global economy.

“Investability” concerns valid, yet overblown

If this is not your brand of whisky, I get it. It’s not for everybody.

The majority of investors today consider China uninvestable and their concerns are valid. Precisely that’s where the opportunity lies—buying outside of foreign / institutional liquidity and selling back into it once the situation improves from terrible to less bad.

Regulation: Jack Ma’s Icarus moment

Regulatory tightening focused on “New Economy” participants—and clustered particularly around antitrust, FinTech / capital markets, data security, and social equality issues—had instilled profound investability concerns among foreign investors even prior to the Russian invasion. It was the scope and length of the regulatory cycle which surprised even the most experienced investors, who know these cycles are not uncommon.

Since June and against all odds, authorities have actually fulfilled their pledges to finalize reforms aimed at “platform companies” (i.e., “New Economy” / Web2). I strongly believe the moderation in regulation intensity we have seen in past months was the main catalyst for the 53% rally off the March lows and continues to support the re-rating of beleaguered ChinaTech equities.

Macro: Bad and better

China’s timid stimulus / policies has been a great source of frustration for investors. Cutting a few points on rates here, injecting a few million there and some mild FX intervention on the side definitely undershot investors' expectations.

My view is that Chinese authorities enjoyed first row seats to the world’s egregious Inflation Show… and hated what they saw.

They postponed expansionary policies until inflationary pressures abate across the world, an easy call for a country with just a 2.8% inflation rate and a perilous real estate situation. If you see your neighbor's beard on fire, water your own.

Geopolitics: China ≠ Russia

There’s no question, the geopolitical situation is perilous. However, we have seen China recently turning colder on Russia, holding back from supplying drones and other military equipment to Russia and publicly voicing “concerns” about Russia’s invasion of Ukraine, which Putin acknowledged. It seems they might be testing the limits of their “unlimited friendship”.

The geopolitical reality can be derived from the excerpt below, included in a previous piece titled $16 ON CHIMERICA & EURUSSIA:

The reality is that China today is the largest trading partner of (checks notes…), basically everyone! We need to acknowledge the emergence of a multipolar world order. Putting our western biases aside for a minute will allow us to perceive the world as it truly is. Rosling. Papic.

This is how I see the situation going forward:

Unlikely widespread support for sanctions against China—it has become “Too Big To Fail” for the global economy, its exports too systemic2

If you didn’t like the impact of Russia’s fallout with the West on inflation, wait to see what happens if you disconnect China; remember: China ≠ Russia

Reasons abound for the West to disapprove of many of China’s policies (i.e., treatment of Uyghur population3, consolidation of Taiwan, tensions in the South China Sea, etc.), but the reality is such "unfair” policies are certainly not uncommon in other parts of the world and do not receive the same treatment by the West / US4

To be clear, I believe today’s hard stance of China will persist as the US comes to terms with Zoltan’s emergence of a multipolar world order5. Prove of that is the recent CHIPS Act, which aims to slow down their perceived opponent while the West retools its economies (i.e., re-arm, re-shore, re-stock and re-wire). But I don’t think the West / US will be able to turn China into the economic pariah Russia is today.

COVID: Reopening Episode IV – A New Hope

With the efficacy of China’s anti-COVID vaccines / pills in doubt and low vaccination rates among the elder, Beijing can only dampen case numbers via rolling lockdowns / closed borders.

To make matters worse, Xi publicly vowed to manage the COVID matter personally, tying his political fate come the 20th NPC—where he “runs” for a third 5Y term—to that of China’s COVID numbers, in a rare act of political ingenuity.

Previously we flagged that “experts [didn’t] expect broad COVID-related restrictions and rolling lockdowns to relax before the 20th NPC held this autumn”. Well, the NPC just concluded and many of us see a chance of Xi quietly claiming victory over COVID and transferring those responsibilities to a scapegoat going forward.

Other relevant developments have been largely overlooked by Western media. China has quietly reduced quarantines in some large cities and is debating the expansion of these reduced quarantines to the rest of the country. The population is starting to protest loudly against restrictions. Seeing leaders meeting / on official events without masks has been a first since the pandemic broke out.

There are reasons to believe China will start to move in this direction—expect to hear more of that going forward. It won’t be noisy, but many of us will watching with great care.

Keep. It. Simple. Part II

I believe things might change in coming months on the re-opening and stimulus front. Do not underestimate the impact of these developments on the global economy—it could be massive.

We have seen China carrying global growth on their shoulders before, what would happen is:

Commodities supercycle turbocharged / extended; where does oil go if China adds 1-2mb/d to today’s demand?

Global economies re-float—particularly China’s largest trading partners in Asia (and the EU)—which would have a large positive impact on FX via shifting surplus / deficit, with the USD taking a large, sustained hit.

If you don’t like prices in 2022, wait to see what happens if China re-opens and pulls its fiscal / monetary levers! A massively inflationary development that could foster higher rates worldwide albeit in a stronger economic environment…

On ChinaTech, I continue to favor the same approach I laid out before:

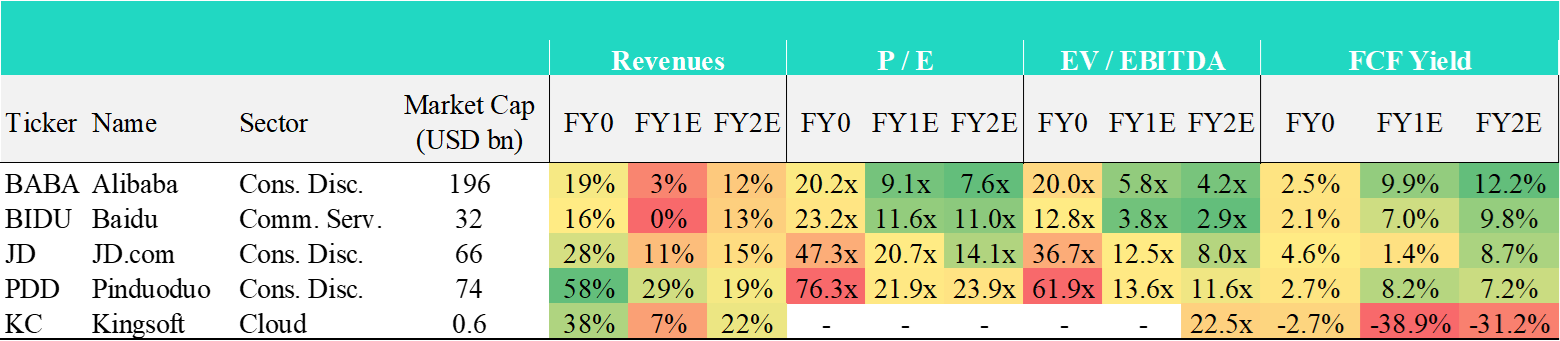

My China tech portfolio is comprised of a majority position in $KWEB—the great, beleaguered proxy for China tech—and a fairly large position in Alibaba ($BABA), surrounded by a constellation of much smaller, different names including Baidu ($BIDU), JD.com ($JD), Pinduoduo ($PDD) and (sometimes) Kingsoft Cloud ($KC). Also, note that roughly 30% of KWEB is composed of those 5 stocks.

I strongly encourage reading the final installment of my ChinaTech series for additional depth. Most hasn’t changed6, including my recommendation to stay cautious and avoid the all-in. I was lucky enough to trade around my positions and pare exposure on the way up, which allowed me to post a small profit on the previous leg and freed capital for the next one. I intend to do the same this time.

I would recommend you to follow me on Twitter if you are interested in seeing the updated metrics for those companies. Find one of the tables below7, the remainder will be shared on Twitter soon.

It’s not the time to be greedy. No fun ‘til the Fed’s done.

$$$

Thanks for reading,

John Galt

PS: Working on a more generalist, earnings-season-centric note, expect it this week. Make sure you subscribe below if you are interested in receiving it first. It’s free. No Spam, ever.

There are strong arguments that suggest the Russia sanctions are a farce, a mere PR stunt by the West. Commodity flows from Russia have not stopped—the majority have simply been re-routed.

Note many muslim countries strongly align with China—including Saudi Arabia, UAE, Turkey—despite the reported human right abuses in the province of Xinjiang. This support partially explains the recent rejection by the U.N. body to debate China's treatment of Uyghur muslims.

I’m not questioning the validity of the West’s disapproval. You name the issue—I will probably agree with most of your points. I also do not believe that the fact that these issues abound lessens their gravity. No question these are all terribly concerning points.

Some might not like this. In a perfect world, policies would be different and the underlying issues wouldn’t exist. But as avid readers have heard me say in the past and in line with Lyn Alden’s recent tweet… I’m an investor. I’m not interested here in what should be, only in what is. I know my German readers will like the next quote, “das Leben ist kein Ponnyhof”.

Finally, not all of china’s policies are terrible. Let’s not forget this is the same country that managed to lift 800 million people out of poverty in the past 40Y, as per the World Bank. The tide has lifted all boats and their population has experienced a quality of life expansion nothing short of a miracle. We’ve seen Nobel prizes being awarded for less.

Refers to Credit Suisse’s Zoltan Pozsar who presented the relevant framework in a missive aptly named “War and Industrial Policy”. I’ve made it available here for you, free.

I recently felt stronger about Kingsoft Cloud—as the price collapsed down to $1.77. I added a small position in the low $2s, which I intend to unwind as the market rebounds. As I explained on Twitter, imagine >$1.3bn in sales trading below net cash.

Edit: MCap and Revenues for FY1E and FY2E corrected for BABA and BIDU since the first version (email) of this piece.