$13 THE BOOK OF MUIR

What if oil stocks have become the tobacco stocks of our generation, the ultimate compounders

Executive Summary

Decade-long structural underinvestment in natural resources and growing global demand conspire in favor of higher prices, a commodities supercycle only to be tamed by capacity expansion / project development or recession

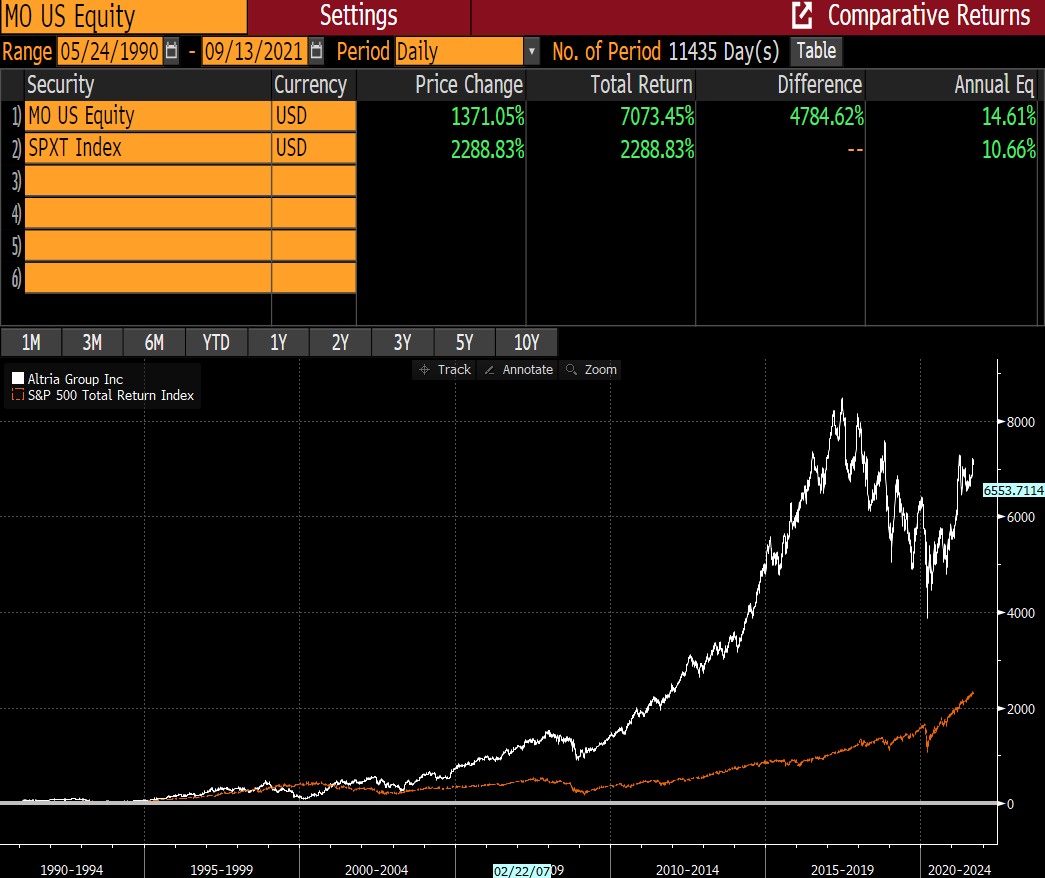

In spite of the institutional capital outflows or rather because of these, tobacco leader Altria has offered a total return ~3x that of the S&P 500 going back to the early ‘90s

“Expect energy companies to become the dividend stocks of our generation, […] great businesses with high yields that institutions don’t want to own”

-$37.63

This subtitle above should suffice for the most acute investors to anticipate where this next post is going.

A barrel. Closing price. April 20, 2020.

By now even those in the investment community who spent the pandemic away from the markets sporting a tinfoil hat know what I‘m talking about.

It was a tumultuous period when investors were presented with the unheralded (unique?1) opportunity to acquire the front-month WTI contract (May 2020) at sub-zero levels. Few did (mercifully, considering the difficulties in securing storage), while many more ventured into the super-contango tanker trade, bought oil-related equities / options / futures or found other, increasingly sophisticated ways to take advantage of the situation.

The problem with opportunities offering exceptional entry points and professional investors is that our investment process often gets in the way of maximizing P&L. We have a tendency to book our profits too early. We get shaken off and then it‘s challenging to jump back in.

Guilty. I owned a portfolio of equity options which I happily cashed out of… and it‘s been difficult for me to develop the required conviction to step back into oil plays at higher levels, despite compelling fundamental arguments and data supporting the contention of an exceptionally strong physical market.

Even for professional investors, quite often it comes down to personal biases, experience and mental accounting.

Now, I’ll tell you who has not been shaken off… or at least retains his position despite a colossal two-year run. Stan Druckenmiller, who delivered the following remarks on June 10:

“The reasons we are still there is we just see this thing being more sustainable because of ESG and all the reasons we all know about. That it can last a while and that doesn’t seem to be priced in the stock. It’s not a typical Duquesne play because it’s now become widely recognized, but I don’t just sell something because. People talk about pain trade, I don’t care about pain trade this or that.

We think these companies are still cheap relative to what we see a year or two out.

The big problem would obviously be if you have a horrendous worldwide recession. We are looking for demand destruction in energy, but so far we don’t see it.”

He’s not the only high-profile investor famously surfing that wave. Warren Buffet (coincidentally) added today 6.7mn shares to its position in Occidental Petroleum ($OXY), where Berkshire’s stake in the common has grown to ~$11.3bn (~20% of the company)2.

He also bought c.20mn shares in Chevron in Q1. Buffet is all in… a depiction he would probably hate.

Well, Mr. Market is kind enough to offer a summer discount from peak levels, as oil prices (West Texas Intermediate, WTI) have corrected 31% and equities—proxied by $XLE, one of the main oil equities ETFs—have careened 21% down from the highs. The spot price is 3% below pre-invasion levels, while XLE trades 11% above.

In the next sections I’ll examine what the oil equities thesis looks like today and borrow a chapter from the Book of Muir3 to expand on the merits of adding oil equities to our long-term / strategic book.

Please note that if you’re buying-a-bunker-in-South-Dakota-bearish about the world and the economy, this is likely not for you. A globally-synchronized recession would (temporarily) trump most fundamentals, as demand contracts steeply and correlations go to 1.

🐐 “All the reasons we all know about”

It’s not a secret that oil companies are doing extraordinarily well—so much so, in fact, that Biden recently proposed a windfall profit tax.

But how did we get here? What are the causes, what Druckenmiller calls “ESG and all the reasons we all know about”?

Everything that is material and not grown must be mined. It’s that simple.

It all starts with a decade-long structural underinvestment in natural resources. As ESG took center stage, capital started to flow out of “non-ESG friendly” sectors. A problem compounded by poor management, wildly dilutive M&A and overall terrible capital allocation. Sources of fresh capital dried up, its cost shot up and projects ceased to be funded. The consequence of that persistent capital starvation are the supply shortages we are experiencing. When COVID broke out, it further constrained supply lines exacerbating the issue.

On the demand side, global population stands at ~8bn and continues growing while demand for a higher standard of living expands rapidly. In the case of oil, daily demand for crude continues to expand—it’s now close to pre-COVID levels—and is projected to continue its uptrend.

All these factors conspire in favor of higher prices in a continued structural upcycle, what many call a commodities supercycle.

When does it end? Well, the only known long-term cure for high prices is… high prices, as these trigger increased supply through capacity expansion / development of new projects and sometimes curtail demand. That or a recession.

The Book of Muir

I admire Kevin Muir and have been a long-time (paid) subscriber to his blog (The Macro Tourist). Back on September 15, he posted a missive under the title TIME TO BUY SOME ENERGY EQUITIES, where he contended that “energy equities are the new tobacco”.

He cited different movements pushing for pension funds / endowments to divest from fossil fuels on his way to building an analogy to tobacco stocks in the early ‘90s.

Now, here comes the important part.

In spite of the institutional capital outflows or rather because of these outflows, “Phillip Morris (Altria for anyone under 50) has returned over 7,000% (it’s important to include dividends in this calculation). The S&P 500, has only returned 2,300%”.

Again, note that the extraordinary performance is not tied to price appreciation, but rather to shareholder remuneration (dividends and share buybacks / repurchases).

Altria has been the ultimate compounder by “targeting an 80% payout ratio of adjusted diluted EPS and has increased and paid a dividend for more than fifty consecutive years”!

Muir goes on to paraphrase a 2015 article by Morgan Housel called “America’s most successful stock”, which identifies the reasons for this outperformance. Again Muir:

According to Morgan, the extraordinary returns of tobacco stocks can be attributed to two factors - both of which resonate with today’s energy story:

1. Fear, disgust & hate. Most investors are like Julio’s-mom-down-by-the-schoolyard and spit on the ground every time energy gets mentioned.

2. Boring is beautiful. Well, energy used to be anything but boring. Yet, given that large amounts of capital are no longer being put to work trying to create innovative new ways to extract oil and nat gas, companies will become more boring than your tenth grade English teacher. They have no choice.

While running some research on Altria, my bud Conor Mac recommended me to check out Devin LaSarre’s work on the company. Devin states that “counter to common belief, regulation is a primary value driver for Altria”, which resonates with Druckenmiller’s assertion on why oil has retained a position in portfolio (“ESG and all the reasons we all know about”).

“The dividend stocks of a generation”

To some this idea may sound provocative. Yet, the reality is that Exxon Mobil ($XOM) and Chevron ($CVX) reported ~$29.5bn in combined profits for Q2 (~$17.9bn and ~$11.6bn, respectively). They are printing money.

Big oil (Exxon, Chevron, BP, Shell & TotalEnergy) dished out more than $20bn on share repurchases in H1 only and will likely surpass these in H2 based on their blockbuster earnings.

Similarly to tobacco firms in the past, these oil companies offer outrageous shareholder remuneration today.

That word is key, today.

Considering the metrics in the table above, I’m inclined to agree with Druckenmiller that these companies remain cheap… if you believe in higher oil prices for longer, this is your bet!

Mr. Market, however, does not believe these earnings will endure. The oil futures strip is backwardated and the price of $XLE relative to the S&P is lagging the upside move in oil. It seems to be factoring in the odds of a recession. This is what you’d be betting against.

Finally a couple of (miscellaneous) thoughts:

Thesis can be played through a combination of companies referenced above or more simply by purchasing the $XLE ETF, which allocates ~23% and ~22% to $XOM and $CVX, respectively.

If you are bearishly positioned, oil equities could be a great hedge not only against inflation, but also for a non-recession scenario.

This thesis could take years to play out in earnest—that’s how compounding works. The entry point matters though and missing exceptional performance early on greatly impacts the longer-term outcome.

This might be another example of an industry moving temporarily outside of institutional liquidity due to “sustainability concerns” to eventually make it back in, as it happens with uranium today. Change is happening—albeit at a slow pace—and oil companies are looking to pivot towards increasingly sustainable / renewable sources of energy / streams of cash flow.

As I explained in $10 IF IT BLEEDS, WE CAN KILL IT, I’m already long energy via uranium, supported by the nascent nuclear revival thesis. To those in my same camp this might offer some diversification for investors seeking energy / commodities exposure.

This fresh perspective encourages me to spend some more time going through the different companies and potentially add it to my long-term / strategic book. In the meantime, I leave you with a final Muir quote that I believe encapsulates beautifully this thesis.

“I think we wake up 5 or 10 years from now, and these hated, dying energy companies will have provided some of the best risk/returns out of the entire stock market universe. […] I expect energy companies to become the dividend stocks of our generation. They will be just like Altria—great businesses with high yields that institutions don’t want to own.”

$$$

Thanks for reading,

John Galt

The term unique gets bandied around too often in the investment world. While I’m often guilty of trafficking in hyperbole myself, I believe this is not such case. Getting paid to buy oil? Come on, give me a break!

From July 18:

Last week, Berkshire Hathaway filed a Form 4 disclosing it purchased another 4.3 million shares of Occidental Petroleum ($OXY) for ~$250 million. Berkshire now owns 179.7 million shares of $OXY, in addition to the Series A Preferred Stock that it acquired through its 2019 agreement with the company (more on this in a moment). At Friday’s close of ~$59 per share, Berkshire’s stake in the common is now worth ~$10.5 billion (~19% of the company).

Not too long ago he delivered some positive comments about the company:

“I would think if you owned Occidental, you’re bullish on oil over the years – and you’re probably bullish on the Permian Basin because they have such a significant portion of their assets there. So, the idea that they will use less stock and more cash as part of the deal… I would think, net, if I had been an $OXY holder at the time, I probably would like that kind of a deal… It’s a bet on oil prices over the long-term more than anything else. It’s also a bet the Permian Basin is what it’s cracked up to be… If oil goes way up, you make a lot of money… You have to have a view on oil over time. Charlie and I have some views on that… We feel good about doing the financing.”

I have a great deal of appreciation for Kevin ‘The Macro Tourist’ Muir, who also co-hosts the Market Huddle . I hope I’ve not butchered his original article / thesis and that none of this is misconstrued. If I chose this title it is because of that admiration for him / his outside-the-box thinking and to give credit where credit’s due.

Great read. I’ve been overweight oil and nuclear for awhile — glad to hear your thoughts on the topic (and Muir’s). My oil positions were not originally intended to be long-term, but I may have to re-evaluate that thesis. Capturing and hanging on to a true compounder is a difficult thing to do — I wouldn’t want to unnecessarily let “let them off the hook” before landing the real returns.